Coordination of Benefits (COB) is the process insurance companies use to determine which health plan pays first (primary payer) and which pays second (secondary payer) when patients have multiple coverages. This prevents duplicate payments and ensures providers receive correct reimbursement. With 43 million Americans covered by multiple health insurance plans, proper COB handling is essential for preventing CO 22 denials—a leading cause of claim rejections that accounts for approximately 10-20% of all denials according to revenue cycle management industry data.

The financial impact hits immediately. Denial rates climbed from 9% in 2016 to 12-15% in 2023 (with private payers at the higher end of that range), and 90% of those denials require human review before resubmission. Each reworked claim costs your organization $25-$60 in administrative expenses, plus the hidden cost of delayed cash flow. For billing departments already stretched thin—with 43% reporting they’re understaffed and 60% managing claims with fewer than 25 people—getting COB right the first time isn’t optional. It’s financial survival.

This guide walks you through everything your billing team needs to master coordination of benefits: the rules that determine payer order, the workflows that prevent denials, the documentation requirements that protect revenue, and the training approaches that scale these processes across growing organizations.

Free: Coordination of Benefits Snippets

Download 14 TextExpander Snippets to help your billing team make the right decisions.

What is Coordination of Benefits in Medical Billing?

Coordination of benefits (COB) is the established process that insurers follow to decide payment order and responsibility when patients carry coverage from multiple health plans. When someone has both their employer’s insurance and coverage as a dependent on their spouse’s plan, or when Medicare beneficiaries maintain group health coverage through continued employment, COB rules determine which insurer processes the claim first and which handles any remaining eligible expenses.

The term itself—coordination of benefits—describes exactly what happens: insurance companies coordinate with each other to determine who covers what portion of a patient’s medical expenses. The alternative would be chaos, with providers submitting the same claim to multiple insurers simultaneously and hoping someone pays. Instead, COB creates a structured sequence where the primary payer processes first, communicates their adjudication decision, and the secondary payer then reviews what remains.

Why does COB matter for revenue cycle operations? Three reasons stand out. First, billing claims to the wrong payer triggers immediate denials, specifically the CO 22 denial code indicating “this care may be covered by another payer per coordination of benefits.” When your registration staff misses a secondary insurance during intake or applies COB rules incorrectly, the claim bounces back unpaid, creating rework for your already-overburdened billing specialists.

Second, COB errors delay reimbursement substantially. Primary payer adjudication takes 15-45 days for most private insurers, with post-service claims typically processed within 30 days under federal ERISA requirements. If you submit to the wrong payer first, you lose those weeks waiting for a denial, then restart the clock submitting to the correct payer. Add secondary payer processing time, and a COB mistake can extend your collection timeline by 60-90 days. For organizations watching cash flow carefully, that delay compounds across dozens or hundreds of claims.

Third, COB complexity increases exponentially as your patient population diversifies. A practice serving mostly commercially-insured adults faces straightforward scenarios. But once you’re treating pediatric patients (triggering birthday rule determinations), Medicare beneficiaries (requiring secondary payer questionnaires), dual-eligible Medicaid patients (adding tertiary complexity), and workers’ compensation cases (introducing yet another payment hierarchy), the cognitive load on your billing team grows dramatically.

The good news? COB follows consistent, learnable rules. Your staff doesn’t need to make subjective judgments about which insurer should pay first. Federal regulations and industry standards establish clear determination methods. The challenge lies in training teams to recognize which rule applies in each scenario, collecting the right documentation upfront, and building workflows that catch mistakes before claims submission—whether you’re handling anesthesia billing,podiatry claims, or general medical services.

For organizations using standardized documentation processes and templates, COB verification becomes faster and more consistent. When your entire registration team follows the same checklist to identify coverage sources and apply determination rules, mistakes drop significantly. The alternative—letting each staff member develop their own approach to insurance verification—creates exactly the variability that leads to CO 22 denials.

How Coordination of Benefits Works: The Complete Process

COB processing follows a structured six-step workflow that touches multiple departments from patient intake through final payment posting. Understanding this complete sequence helps billing managers identify where breakdowns occur and where process improvements deliver the highest return.

The first step happens at patient registration, ideally before services are even rendered. Your front desk staff collects insurance cards for all active policies the patient maintains. This means explicitly asking whether they have coverage through their own employer, a spouse’s employer, Medicare, Medicaid, workers’ compensation, or auto insurance if the visit relates to an accident. The most common COB error? Assuming a patient has only one insurance because they present only one card. Train your registration team to ask directly: “Do you have any other health insurance coverage besides this policy?”

Once you’ve identified all active policies, verify current eligibility electronically for each one. Eligibility responses often include a COB indicator showing whether other coverage exists and may even identify the other payer. Don’t skip this step thinking you’ll catch problems later. Electronic eligibility verification catches expired policies, coverage gaps, and COB scenarios in real-time, before you’ve provided services and invested effort in claim preparation.

Document the policy holder relationship for each plan. Is the patient the primary subscriber, or are they covered as a spouse or dependent child? This detail drives COB rule application. Your practice management system should capture this relationship clearly—not buried in free-text notes where billing staff must hunt for it, but in dedicated fields that populate claim forms automatically.

Step two requires determining primary versus secondary payer using established COB rules. We’ll detail these rules extensively in the next section, but the key point here is documentation. When your staff determines payer order, that decision should be recorded clearly in the patient account with rationale. “Primary: Aetna per birthday rule (subscriber DOB 3/15)” tells your billing team exactly why this determination was made and provides an audit trail if questioned later.

Update your billing system with the correct payer order—marking policies as primary, secondary, or tertiary. Most practice management systems use numeric indicators: 1 for primary, 2 for secondary, 3 for tertiary. Configure these correctly before anyone starts working claims, because reversing payer order after initial submission creates compounding delays.

Step three is claim submission to the primary payer. This follows your standard clean claim submission workflow through your clearinghouse, with all required documentation and any prior authorization confirmations attached. The only COB-specific requirement at this stage: make absolutely certain you’re actually submitting to the primary payer. This seems obvious, but when staff are rushing through high claim volumes, mistakes happen. Many organizations build a final verification step where a second person spot-checks payer order on accounts flagged as having multiple insurances.

Track your timely filing deadlines religiously. Most private insurers allow 90 days from date of service. Medicare allows up to one year. Medicaid timelines vary by state. When you’re coordinating benefits, you’re managing multiple timely filing deadlines—one for each payer in the sequence. Missing the primary payer’s deadline because you didn’t realize they were primary means you’ve lost that revenue entirely. Missing the secondary payer’s deadline after the primary has paid means leaving money on the table.

Step four is receiving and processing the primary payer’s Explanation of Benefits (EOB). Your payment posting team applies the primary payment to the patient account, records contractual adjustments per your agreement with that insurer, and calculates remaining patient responsibility. Here’s where many organizations lose track of COB processing: they post the primary payment, see a remaining balance, and immediately send a patient statement without checking whether secondary insurance should be billed next.

Build a workflow rule: accounts with multiple active insurances don’t generate patient statements until all insurance processing completes. You can implement this as a hard stop in your practice management system, a daily report of accounts needing secondary submission, or training your payment posting staff to check insurance coverage before releasing patient bills. Pick whatever method fits your systems, but make it automatic rather than relying on staff to remember.

Step five is submitting the secondary claim with the primary payer’s EOB attached. This is where CO 22 denials occur most frequently. Secondary payers need to see what the primary payer paid, adjusted, and determined as patient responsibility before they can adjudicate their portion. Submit a secondary claim without the primary EOB, and you’ll receive a denial requesting that documentation. This seems like a minor procedural requirement, but it adds weeks to your collection timeline and creates yet another task for your denial management team.

Your clearinghouse should handle EOB attachment electronically for secondary claims, pulling the 835 remittance data from the primary payer and including it in the secondary submission. If you’re still dealing with paper EOBs, scanning and attaching them manually, you’re spending far more time on COB processing than necessary and increasing your error rate substantially.

Calculate the remaining balance carefully before secondary submission. Don’t just bill the secondary payer for everything the primary didn’t pay. Bill them for the remaining allowed amount after primary payment, excluding contractual adjustments that aren’t transferable to secondary coverage. Your practice management system should calculate this automatically if payer relationships are configured correctly.

Step six applies when tertiary insurance exists, typically in Medicare-Medicaid dual-eligible scenarios. Follow the same process: receive the secondary payer’s EOB, post their payment and adjustments, then submit remaining balance to the tertiary payer with both previous EOBs attached. The complexity compounds, but the process remains consistent.

After all insurance processing completes, generate your patient statement for any remaining balance. This is true patient responsibility—the amount that multiple insurers have determined the patient must pay based on their coverage terms.

How long does this complete sequence take? Plan on 15-45 days for primary payer adjudication depending on claim type—post-service claims typically process within 30 days under federal ERISA requirements, with possible 15-day extensions for complex cases. Add another 14-21 days for secondary processing. Medicare moves faster (often 14 days for electronic claims), while some commercial payers stretch toward the 45-day maximum. Tertiary processing adds another 2-3 weeks. A complex dual-eligible claim with all payers involved can run 60-90 days from submission to final resolution.

This extended timeline explains why COB errors hurt so much. Make a mistake on day one, receive a denial on day 21, correct and resubmit on day 23, and you’re looking at day 44 before the claim even begins proper processing. That’s six weeks of float time where your organization has provided services, incurred costs, and received nothing—all because someone missed a checkbox during patient registration.

For organizations managing dozens of these workflows simultaneously, standardized templates for insurance verification help ensure the same quality approach every time. When your registration staff uses consistent COB documentation, your billing specialists can trust the payer order determination without re-verifying everything. This trust speeds processing and lets staff focus on genuinely complex cases rather than checking everyone’s work.

Stop COB Denials Before They Start

Give your billing team instant access to insurance verification checklists, COB rule references, and payer-specific requirements. TextExpander ensures consistent documentation across 100+ person departments.

Primary vs Secondary Insurance: COB Rules Explained

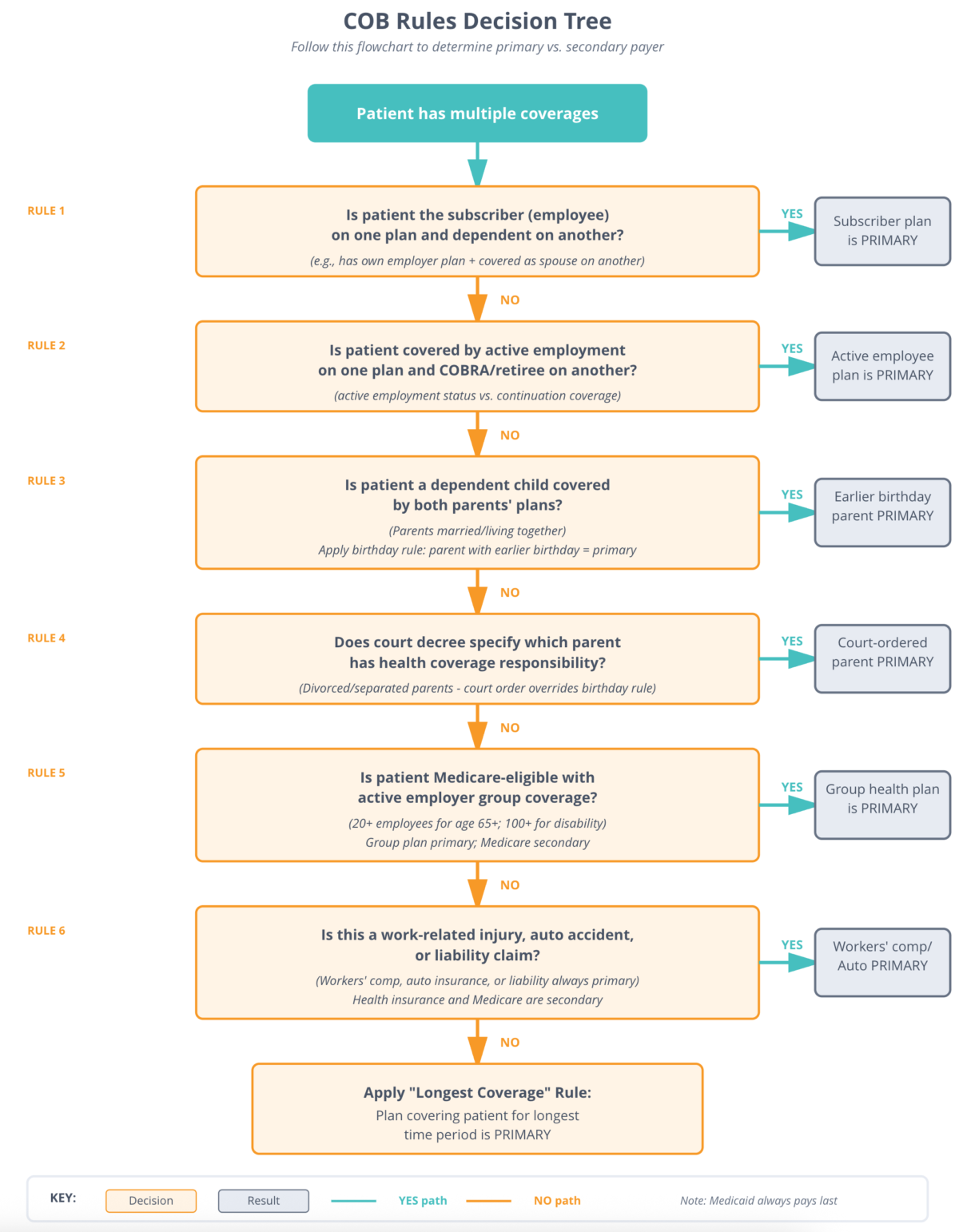

Five core rules determine payer order in virtually every COB scenario your billing team encounters. Master these rules and you eliminate the guesswork that creates claim denials.

The birthday rule determines coverage order for dependent children covered by both parents’ health plans. When parents are married and living together, the parent whose birthday falls earlier in the calendar year holds the primary plan for their children. Notice what the rule considers: birthday month and day only, not year of birth. If Dad’s birthday is January 25, 1985 and Mom’s birthday is July 15, 1990, Dad’s plan is primary despite being older. Only the month and day matter—January comes before July.

Why does this rule exist? Before standardization, insurance companies applied different determination methods, creating disputes and delays when both parents’ plans covered children. The National Association of Insurance Commissioners established the birthday rule to eliminate this variability. Now every major insurer follows it uniformly, making determinations predictable and straightforward.

Two important exceptions to the birthday rule require attention. First, when parents are divorced or legally separated, the birthday rule doesn’t apply. Instead, custody arrangements drive the determination. The custodial parent’s plan covers the child primarily, the non-custodial parent’s plan pays secondary, and any plan covering a stepparent pays tertiary. Court-ordered responsibility stated in divorce decrees supersedes all other rules—if the divorce agreement specifies which parent’s insurance must be primary, that determination stands regardless of birthday or custody.

Second, some states have enacted their own COB rules that override the birthday rule. These state-specific variations are rare but exist. Your billing staff should understand which states you serve and whether any maintain non-standard COB determination methods. Don’t assume the birthday rule applies universally without verifying.

The active versus inactive employee rule resolves conflicts when one insurance plan covers someone through active employment and another covers them as a retiree or through COBRA continuation coverage. Active employment coverage always pays before retiree or COBRA plans. This makes intuitive sense: current group coverage takes precedence over continuation benefits tied to former employment.

This rule extends to Medicare coordination for working-aged beneficiaries. If someone qualifies for Medicare at age 65 but continues working with employer group health coverage (from an employer with 20 or more employees), that employer plan pays primary and Medicare pays secondary. Once they retire and lose that active coverage, Medicare becomes primary for any remaining coverage they maintain.

Medicare representatives often explain this simply to beneficiaries: “If you’re still working and have insurance through your job, we’re your backup.” But billing staff need more precision than that. The 20-employee threshold matters—small employer plans don’t have the same primary responsibility. And “working” means actively employed, not just health coverage purchased through a former employer. A 67-year-old with Medicare who buys COBRA from their former employer makes Medicare primary because COBRA is continuation coverage, not active employment benefits.

The self versus dependent rule applies when someone has coverage both as a subscriber on their own plan and as a dependent on someone else’s plan—typically when one spouse has their own employer coverage but also qualifies for coverage as a dependent on their spouse’s plan. The plan where the person is the primary subscriber pays first. The plan where they’re listed as a dependent pays second.

This rule seems straightforward, but creates confusion when spouses work for the same employer. If both spouses work at the same company and that company’s health plan allows employees to cover their working spouses, who’s primary for whom? The answer: each person’s primary coverage is the plan where they’re the employee, not the dependent. Husband covered through his own employment with Company A is primary for himself even if his wife also works for Company A and could cover him as a dependent.

Medicare secondary payer rules deserve special attention because Medicare coordination scenarios are common and the rules are complex. When Medicare beneficiaries maintain other coverage, federal law establishes a strict payment hierarchy that protects Medicare from paying amounts other insurers should cover.

For beneficiaries under age 65 who qualify for Medicare due to disability, large group health plans (covering employers with 100+ employees) pay primary to Medicare. Once they turn 65, the employer size threshold drops to 20+ employees. These thresholds reflect federal policy decisions about when employers must maintain primary payment responsibility versus when Medicare can reasonably expect to pay first.

End-stage renal disease (ESRD) creates a time-limited coordination period. When someone newly diagnosed with ESRD becomes Medicare-eligible, any existing group health plan remains primary for the first 30 months of Medicare eligibility. After 30 months, Medicare becomes primary. This coordination period gives patients time to adjust while protecting group plans from immediate full financial responsibility for ongoing dialysis costs.

Workers’ compensation and auto insurance always pay primary to Medicare for services related to work injuries or auto accidents. This isn’t negotiable—Medicare specifically excludes coverage of services that another payer is legally obligated to cover. If a Medicare beneficiary receives treatment for injuries from a car accident and Medicare processes the claim first, Medicare may later pursue recovery from the auto insurer once that payer is identified.

No-fault auto insurance and liability insurance must pay before Medicare processes claims. This creates complexity for billing staff because patients may not immediately disclose accident-related circumstances, especially for delayed symptom development. Train your registration teams to ask specifically about recent accidents or injuries when Medicare beneficiaries present for treatment of symptoms that could relate to traumatic incidents.

The Medicare Secondary Payer questionnaire exists specifically to identify these coordination scenarios. Federal regulations require all Medicare providers to complete this questionnaire and update the information periodically. Failure to complete MSP questionnaires properly can result in Medicare denial of claims that should have been processed, or worse, Medicare paying first and later pursuing recovery from your organization when it’s determined another payer should have been primary.

The fifth rule is simple but absolute: Medicaid always pays last. When patients qualify for both Medicare and Medicaid (the 12.8 million dual-eligible beneficiaries in the United States), Medicare processes first as the primary payer, then Medicaid covers applicable copayments, coinsurance, and deductibles as the secondary payer. Medicaid serves as the true payer of last resort in the American healthcare system.

For dual-eligible beneficiaries, this coordination happens largely automatically through data exchanges between CMS and state Medicaid programs. But providers must still submit claims correctly—billing Medicare first, receiving that EOB, then submitting to Medicaid with Medicare’s payment information included.

When commercial insurance exists alongside Medicare and Medicaid, the sequence extends: commercial insurance first, Medicare second, Medicaid third. Each payer reviews the remaining balance after the previous payer’s adjudication, applies their coverage rules, and either pays a portion or denies if their policy doesn’t cover remaining amounts.

Why does payer order matter so precisely? Because insurance companies don’t just want to avoid paying claims others should cover—they’re legally bound by coordination of benefit rules established through federal regulation and state insurance department oversight. When you submit claims in the wrong order, payers deny them with specific reason codes directing you to bill the correct primary payer. These aren’t arbitrary requirements your staff can work around through persistence or appeals. They’re established rules that must be followed.

High-performing billing departments document these rules clearly and make them instantly accessible to staff. Rather than requiring billers to memorize all scenarios or hunt through policy manuals each time a question arises, organizations create quick-reference guides covering the most common situations. Tools like standardized COB decision trees and rule explanations ensure every team member applies rules consistently regardless of their experience level.

Common COB Scenarios in Medical Billing

Understanding COB rules abstractly is one thing. Recognizing them in real patient situations is another. These scenarios illustrate how billing specialists apply determination rules to actual cases walking through your door every day.

Sarah, age 68, worked for a large telecommunications company until last year. She enrolled in Medicare at 65 but kept working and maintained her employer group health coverage. During those three years of simultaneous coverage, her employer plan paid primary and Medicare paid secondary because she was actively employed with a large employer. Last year she retired but immediately took a part-time position with a different company that offers group health coverage. The new employer is smaller—only 18 employees. For claims related to this new employment, Medicare now pays primary because the employer doesn’t meet the 20-employee threshold that triggers primary payment responsibility. For Sarah’s billing team to process her claims correctly, they need to know her employment status, her employer’s size, and which coverage relates to which employment. A single checkbox error in the practice management system could reverse this coordination and trigger automatic denials.

Michael and Jennifer both work full-time and maintain separate employer-sponsored health plans. They’ve enrolled their three children on both plans to maximize coverage. When their 8-year-old daughter Emma visits the pediatrician, which insurance should the office bill first? Michael’s birthday is February 10, and Jennifer’s birthday is August 22. Under the birthday rule, Michael’s plan is primary for all three children because February comes before August in the calendar year. The office bills Michael’s Anthem plan first, receives an EOB showing Anthem’s payment and allowed amounts, then bills Jennifer’s Cigna plan with that EOB attached for any remaining patient responsibility. If Emma requires significant medical care throughout the year, the secondary insurance may cover most or all copayments and deductibles that the primary plan didn’t pay, substantially reducing the family’s out-of-pocket costs. But none of that secondary payment happens if the office doesn’t bill the secondary insurer or bills the wrong insurer first.

Robert, age 70, receives Medicare and also qualifies for Medicaid benefits based on income. He visits the emergency department for chest pain and receives extensive cardiac workup including EKG, cardiac enzymes, imaging, and observation services. The hospital’s billing sequence: submit to Medicare first as the primary payer, receive Medicare’s payment covering approximately 80% of allowed amounts, then submit to Medicaid with Medicare’s EOB attached. Medicaid reviews the remaining balance and covers Robert’s Medicare Part A and Part B premiums, deductibles, and coinsurance according to their crossover agreement. Robert receives care without any patient responsibility. The hospital receives full payment only because they correctly coordinated both payers in proper sequence.

Lisa recently divorced after 15 years of marriage. Her 12-year-old son Daniel is covered by both parents’ health insurance. The divorce decree specifies that Lisa has physical custody during the school year and her ex-husband has summer custody. More importantly, the divorce agreement states that the father is responsible for maintaining health insurance for Daniel and covering all medical expenses. When Daniel breaks his arm skateboarding during the school year, which insurance pays first? Despite the birthday rule existing, court-ordered responsibility supersedes it. The father’s insurance is primary per the divorce decree, even though Daniel was living with Lisa at the time of the injury and even if Lisa’s birthday came earlier in the year than her ex-husband’s. The medical office must document this court-ordered responsibility carefully and bill according to the legal agreement rather than standard COB rules.

Patricia, age 45, qualifies for Medicare due to end-stage renal disease. She’s been on dialysis for 15 months and continues working full-time with employer group health coverage through her company of 200+ employees. For her dialysis treatments and ESRD-related care, her employer plan pays primary because she’s within the 30-month coordination period that federal law establishes for ESRD patients. When month 31 arrives, Medicare automatically becomes primary for all services, and Patricia’s employer plan becomes secondary. The dialysis center’s billing team must track this 30-month window carefully because missing the transition date means submitting claims to the wrong primary payer and receiving automatic denials. Many dialysis centers maintain spreadsheets or calendar reminders tracking their ESRD patients’ coordination periods to avoid this specific mistake.

David, age 63, injured his back at work and filed a workers’ compensation claim. He also maintains commercial health insurance through his employer. He visits his primary care physician for ongoing back pain related to the work injury. The physician’s office must determine whether this visit relates to the work injury (making workers’ compensation primary) or represents different care (making his regular health insurance primary). They review David’s workers’ comp authorization and confirm the visit is approved for work-related follow-up care. Workers’ compensation pays primary for this visit. If David later sees the same physician for unrelated conditions like annual physicals or sick visits for flu, those visits bill to his regular health insurance because they’re not work-related. The office maintains careful documentation about which services relate to the work injury versus David’s other health needs.

These scenarios share common threads. First, proper COB requires information collection at registration. You can’t apply birthday rules if you don’t ask about both parents’ birthdays. You can’t coordinate Medicare with employment-based coverage if you don’t ask about current employment status and employer size. Train registration staff to gather COB-relevant information systematically, not just when they remember to ask.

Second, COB determinations require documentation. When your billing specialist determines which insurance is primary, document why. “Primary per birthday rule,” “Primary per active employment,” “Primary per divorce decree dated 3/15/2023” gives your team and any auditors clear rationale for billing decisions.

Third, these scenarios show how COB errors aren’t just abstract billing problems—they represent real delays in provider payment and potential balance-billing disputes with patients who don’t understand why they’re receiving bills they thought insurance covered. Get coordination right and patient satisfaction improves alongside your collection rates. Get it wrong and you’re explaining to frustrated patients why their insurance didn’t pay as expected.

Training staff on these scenarios? Download our COB scenario reference library →

COB-Related Denial Codes and Prevention

Coordination of benefits errors manifest as specific denial codes that signal billing mistakes your team must correct. Understanding what triggers these denials and how to prevent them protects your revenue cycle from systematic delays.

Denial code CO 22 appears on remittance advice with the description “This care may be covered by another payer per coordination of benefits.” This denial means the payer you submitted to has information indicating they’re not the primary payer responsible for this claim. They’re declining to process it and directing you to bill the correct primary payer first.

CO 22 denials stem from three root causes. First, the payer’s eligibility system shows the patient has other coverage that should pay primary. Perhaps their database indicates the patient has Medicare, workers’ compensation, or another commercial plan that takes precedence under COB rules. Second, the patient informed the payer about other coverage that you didn’t bill first. Insurance companies periodically send coordination of benefits questionnaires to members asking about other health coverage. If a patient reports they have multiple insurances and you billed the wrong one first, CO 22 denial follows. Third, previous payment patterns triggered the denial. If this patient’s claims always bill to Plan A first, then suddenly you submit directly to Plan B, the system flags this as a potential COB error.

Preventing CO 22 denials requires accurate upfront verification. During patient registration, explicitly ask about all active health insurance coverage. Don’t rely on patients volunteering this information—many don’t realize it’s relevant. Use specific questions: “Do you have any other health insurance besides this policy? Are you covered through your spouse’s employer? Do you have Medicare? Are we seeing you for an injury that might be covered by workers’ compensation or auto insurance?”

Verify eligibility electronically for all policies the patient mentions. Most eligibility responses include COB indicators showing whether other coverage exists and sometimes identifying the other payer. This real-time verification catches discrepancies before you invest time in claim preparation and submission.

Document your COB determination clearly in the patient account. Don’t just mark one insurance as primary and another as secondary. Record why: “Primary = Aetna per birthday rule, secondary = BCBS.” This documentation helps billing staff months later when they’re working a denial and need to understand the original determination logic.

Denial code PR 31 reads “Patient cannot be identified as our insured.” While not exclusively a COB code, PR 31 appears frequently in coordination scenarios when subscriber identification gets mixed up between multiple policies. If you’ve transposed subscriber information from the primary plan onto the secondary claim, or used the wrong policy number for the payer you’re billing, PR 31 rejection follows.

This error occurs most often when family members are subscribers on different policies and your staff must track which family member is the subscriber for which payer. Dad is the subscriber on policy A, Mom is the subscriber on policy B, and the children are dependents on both. Bill policy A with Mom’s subscriber information or policy B with Dad’s subscriber information and the claim rejects because the payer can’t identify the patient under that subscriber’s policy.

Prevention means meticulous data entry and verification. When patients present multiple insurance cards, your registration team must record each policy’s subscriber name, relationship to patient, and policy number accurately. Double-check this information against what the insurance cards actually show. If your practice management system allows, require staff to enter a patient’s relationship to the subscriber (self, spouse, child, other dependent) which helps catch mismatches before submission.

Other COB-related denials include claims missing required EOB attachments when billing secondary payers. The denial might state “additional information required” or “missing coordination of benefits documentation.” These denials are entirely preventable. Your claims workflow should automatically attach the primary payer’s 835 remittance data to secondary claims. If you’re still managing paper EOBs, implement scanning procedures that attach these documents before secondary submission.

Timely filing denials occur more frequently in COB scenarios because each payer has separate filing deadlines. If the primary payer takes 28 days to adjudicate, then you spend 3 days posting that payment and preparing the secondary claim, then the secondary claim sits in your clearinghouse queue for 2 days before actually transmitting, you’ve used 33 days of your secondary payer’s timeline before they even receive the claim. Most secondary payers allow 90-120 days from the primary payer’s payment date, but verify each payer’s specific requirements. Missing timely filing deadlines for secondary claims means leaving money on the table—amounts the primary payer didn’t cover but the secondary would have paid if you’d submitted within their deadline.

Track COB-related denials systematically. Pull monthly reports showing all claims denied with CO 22, PR 31, and COB-related reason codes. Calculate what percentage of your total denials these represent. For organizations with significant dual-coverage patient populations, COB errors can account for 5-10% of all denials. That’s substantial when each denial costs $25-$60 to correct and resubmit according to industry analyses.

Analyze patterns in your COB denials. Are certain staff members generating more CO 22 denials than others? That signals training needs. Are denials concentrated among specific payers? That might indicate you need clearer documentation of that payer’s specific COB requirements. Are denials occurring primarily for certain service types like emergency department visits where patients often can’t provide complete insurance information upfront? That suggests you need better processes for following up on incomplete registrations.

The financial impact of COB-related denials extends beyond rework costs. According to industry research, organizations experiencing high denial rates see their days in accounts receivable climb by 15-20 days on average. When you’re floating 60-90 days of revenue instead of 45 days because of preventable denials, that’s working capital tied up unnecessarily.

For departments managing hundreds of claims daily, preventing COB denials requires systematic approaches. Training helps, but training alone doesn’t prevent mistakes when staff are rushed or tired. Procedural controls—required fields, verification steps, system edits—catch errors at the point of entry before they become claim submissions. Standardized verification checklists that registration staff complete for every patient with multiple insurances ensure the same thorough approach regardless of volume pressures or individual staff variations.

COB Documentation Requirements

Proper coordination of benefits processing depends on collecting specific information during registration and maintaining that documentation throughout the claim lifecycle. Missing even one data element can trigger denials that delay payment by weeks or months.

At patient registration, your team needs complete information about every active insurance policy. For each policy, collect the insurance card (front and back), photograph or scan the card so you have a permanent record, record the policy holder’s full name exactly as it appears on the card, document the policy holder’s relationship to the patient (self, spouse, child, other), record the policy holder’s date of birth if the patient is a dependent child, note the group number and subscriber ID, record the effective date of coverage, and document contact information for claims submission.

Don’t accept incomplete information. When patients say “I have insurance but don’t have my card with me,” get what information they can provide immediately, then flag the account for follow-up before claim submission. Many practices now require patients to provide current insurance information at every visit, not just at initial registration, because insurance changes frequently and outdated information is one of the leading causes of claim denials.

Document the COB determination and rationale. When your registration staff determines which insurance is primary, record that decision in the patient account along with the reasoning: “Primary: Aetna per birthday rule (subscriber DOB 3/15), Secondary: UHC” provides clear documentation that supports the claim if questioned later. This notation takes 30 seconds to enter but saves substantial time when billing staff work the account weeks later and need to understand why payers were ordered this way. When communicating these determinations to patients, standardized patient email templates ensure consistent, professional messaging.

For Medicare beneficiaries, complete the Medicare Secondary Payer (MSP) questionnaire. Federal regulations require all Medicare providers to ask these questions and document responses. The questionnaire identifies whether Medicare should pay primary or secondary based on factors like current employment, employer size, disability status, ESRD treatment, or work-related injury. Medicare maintains a database of this information and matches it against incoming claims. If their records indicate another payer should be primary but you bill Medicare first, the claim denies automatically.

Update MSP information periodically. Medicare requires providers to check MSP status at least annually and whenever the patient reports a significant change like retirement, new employment, or changes in spouse’s employment. Many practices integrate MSP questions into their annual patient information update process, ensuring they’re re-verifying this crucial coordination information systematically.

When submitting secondary claims, attach the primary payer’s Explanation of Benefits. This can be the electronic 835 remittance data or a scanned paper EOB if the primary payer doesn’t provide electronic remittances. The secondary payer needs to see what the primary payer allowed, paid, adjusted, and determined as patient responsibility before they can adjudicate their portion. Submit a secondary claim without this documentation and you’re virtually guaranteed a denial requesting it.

Include specific coordination information in the claim itself. The HIPAA 837 electronic claim format includes Loop 2330 specifically for coordination of benefits information. This section indicates whether other coverage exists, identifies the other payer, and provides the other policy information. Fill these fields accurately when submitting to the primary payer (indicating secondary coverage exists) and when submitting to the secondary payer (identifying the primary payer and that they’ve already adjudicated).

Maintain complete documentation throughout the claim lifecycle. When you receive denials related to coordination issues, document the denial reason code, what corrective action you took, and when you resubmitted. If you contact a payer for clarification about COB requirements, document that conversation including date, time, representative name, and what they instructed you to do. This documentation protects your organization if payment delays or if you need to appeal a denial.

For accounts with tertiary insurance, documentation complexity increases because you’re managing three separate adjudications. Maintain clear records of the processing sequence: primary payer paid date and amount, secondary payer paid date and amount, remaining balance submitted to tertiary. This timeline documentation helps your AR follow-up team track where each claim stands in the multi-payer processing sequence.

The documentation burden might seem excessive, but it’s proportional to the complexity COB introduces to revenue cycle operations. When single-insurance claims move through in 2-4 weeks with minimal touches, but COB claims require 6-12 weeks with multiple follow-ups and potential appeals, that additional documentation becomes the only way to maintain control and visibility over these extended collection timelines.

Organizations managing large volumes of dual-coverage patients often standardize their COB documentation using templates and checklists. When every staff member follows the same documentation format and captures the same data points, downstream processing becomes more efficient because billers know exactly where to find needed information. Shared knowledge management systems ensure institutional knowledge about specific payers’ COB requirements doesn’t reside in individual staff members’ heads but exists in documented, searchable formats accessible to everyone who needs it.

See how affordable better documentation consistency can be

TextExpander costs just a few hundred dollars annually. Compare that to the $25-50 you’re spending to rework each denied claim, and the ROI becomes immediate.

COB Verification Best Practices

Preventing coordination of benefits errors requires systematic approaches built into your registration and billing workflows. These best practices help organizations manage COB complexity without overwhelming staff.

Verify all coverage sources at every patient encounter, not just during initial registration. Insurance changes frequently—patients switch jobs, add coverage through spouses, gain or lose Medicare eligibility, or modify their benefits during open enrollment periods. A patient who presented with single coverage six months ago might now have dual coverage, but your staff won’t know unless they ask. Make insurance verification a required step at every visit, including established patients.

Use automated eligibility checking tools for real-time verification. Electronic eligibility verification returns responses in seconds and often includes coordination of benefits indicators showing whether other active coverage exists. This immediate feedback catches potential COB issues before you’ve provided services or invested time in documentation. Most practice management systems integrate directly with eligibility verification vendors, making this step nearly effortless for registration staff.

Ask specific questions about other coverage. Generic questions like “Has anything changed with your insurance?” miss many coordination scenarios because patients don’t realize what information is relevant. Instead, ask: “Are you covered by any other health insurance plans besides this one? Do you have Medicare? Are you covered under your spouse’s plan? Is this visit related to a work injury or auto accident? Did you recently retire or change jobs?” Specific questions yield specific answers that reveal COB scenarios.

Train registration staff to recognize high-risk COB scenarios. Patients under age 26 might be covered under parents’ insurance plus their own employer plan. Patients aged 65-70 often have both Medicare and employment-based coverage. Married patients frequently have dual coverage through their own employer and their spouse’s. Emergency department visits might involve auto insurance or workers’ compensation. When staff recognize these patterns, they know to probe deeper about additional coverage.

Flag accounts with multiple insurances for billing team review. Your practice management system should clearly mark these accounts so billing specialists know to pay extra attention to payer order verification before claim submission. Some organizations implement a two-person verification process where a second staff member spot-checks payer order on all flagged accounts before transmission. This catches determination errors before they become denials.

Create payer-specific COB requirement documentation. Major insurance companies often have unique coordination rules or documentation requirements beyond standard industry practices. Some payers want secondary claims submitted separately rather than automatically crossing over from primary adjudication. Others require specific authorization procedures when processing as secondary. Document these payer-specific requirements in your knowledge base so staff can reference them when working these accounts.

Monitor your CO 22 denial rate monthly. Calculate what percentage of your total denials are coordination-related. For most organizations, this should be under 2-3% of total denials. If you’re seeing 5% or higher, COB errors represent a systematic problem requiring focused improvement efforts. Break down CO 22 denials by staff member to identify training needs and by payer to identify whether specific insurers are declining your claims for coordination reasons more often than others.

Review denied claims immediately. Don’t let COB denials sit in work queues for days or weeks before someone addresses them. Every day of delay compounds the cash flow impact. Assign denied claims to experienced staff who can quickly identify the issue, obtain needed documentation, and resubmit correctly. Organizations with high COB patient volumes sometimes designate specialists who handle only coordination-related denials, building deep expertise in resolving these specific issues.

Build systematic appeals processes for disputed COB determinations. Sometimes payers deny claims as secondary when your documentation clearly supports primary coverage. Don’t accept these denials without question. Prepare appeals including: a clear written explanation of why your COB determination is correct, copies of both insurance cards showing effective dates, documentation supporting the applicable rule (birth dates for birthday rule, employment verification for active/inactive determinations, etc.), and copies of eligibility verifications from both payers if available. Well-documented appeals overturn many incorrect COB denials.

Educate providers about documentation requirements that support COB processing. Physicians and other clinical staff may not realize how their documentation affects claim processing. When they don’t clearly document whether an injury is work-related or accident-related, that creates ambiguity about whether workers’ compensation or auto insurance should be billed. When they don’t document Medicare patients’ employment status, that makes it harder for billing staff to determine Medicare secondary payer status. Regular feedback from billing to clinical teams about documentation gaps improves the information available for COB determinations.

Use technology appropriately but don’t expect it to solve coordination problems automatically. Practice management systems can store multiple insurance policies, mark payer order, and even apply some basic business rules about COB. But they can’t interview patients to discover undisclosed coverage, can’t evaluate employment status to determine active versus inactive rules, and can’t read divorce decrees to identify court-ordered insurance responsibility. Technology supports human decision-making in COB scenarios, it doesn’t replace it.

For organizations managing tens of thousands of patient accounts with varying insurance combinations, building these systematic approaches into standard workflows becomes critical. Billing training programs that emphasize COB scenarios help new staff recognize coordination situations faster. Ongoing education about payer-specific requirements keeps experienced staff current as insurance company policies evolve. And standardized tools that make institutional knowledge immediately accessible to everyone prevent the knowledge silos that create inconsistent COB handling across shifts and locations.

Training Your Team on COB

Effective coordination of benefits processing requires specialized knowledge that most billing staff don’t bring from previous positions. Even experienced billers who understand COB conceptually need training on your organization’s specific workflows, payer mix, and documentation requirements.

Start with COB fundamentals for all registration and billing staff. Everyone who touches patient accounts should understand that multiple insurances exist, why payer order matters, and the financial consequences of COB errors. You’re not teaching registration staff to be expert billers, but they need enough foundation to collect the right information upfront. Cover: what coordination of benefits means and why it exists, how multiple insurances pay sequentially rather than simultaneously, the basic concept of primary versus secondary payers, why insurance cards contain policy holder information and how to read it, and what information registration must collect to support downstream COB processing.

Teach the five core COB rules explicitly. Don’t expect staff to piece together birthday rules from random examples. Present each rule formally: the birthday rule and its exceptions, the active versus inactive employee rule, the self versus dependent rule, Medicare secondary payer rules, and Medicaid always paying last. For each rule, provide the specific decision criteria and work through 3-4 examples showing the rule in application. This structured approach builds mental models staff can apply when encountering new scenarios.

Use case studies and scenarios for practice. After presenting each rule, work through examples together: “Patient is a 10-year-old with coverage from both parents. Dad’s birthday is May 3, Mom’s birthday is October 12. Which insurance is primary?” Let staff work through the logic themselves with guidance. This active learning cements understanding better than passive listening.

Address common mistakes explicitly. Collect examples of actual COB errors that have occurred in your organization—registrations that missed secondary insurance, claims submitted to the wrong primary payer, missing EOB attachments on secondary claims. Present these as learning examples during training. Seeing real mistakes with real consequences helps staff understand why the requirements exist and what happens when procedures aren’t followed carefully.

Create role-specific training focusing on what each position needs to know. Registration staff need deep knowledge of information collection and initial COB determination but don’t need to understand secondary claim submission mechanics. Billing specialists need thorough understanding of claim preparation and submission requirements but may not need the same detail about how to interview patients. Payment posting staff need to recognize when EOBs indicate coordination issues that require follow-up. Denial management staff need expertise in researching and resolving COB errors. Tailor training to these specific responsibilities rather than teaching everyone everything.

Develop quick reference materials staff can consult during daily work. COB rules aren’t intuitive enough that most people remember them perfectly after initial training. Create decision trees: “Is the patient a dependent child covered by both parents? → Yes → Are parents married and living together? → Yes → Apply birthday rule.” These visual guides support staff making real-time determinations without having to remember every detail from training weeks or months earlier.

Implement supervised practice periods for new staff. After classroom-style training on COB concepts, new staff need opportunities to apply this knowledge with oversight. Have them work accounts with experienced staff reviewing their determinations and providing immediate feedback. This supervised practice identifies misunderstandings before they become systematic errors in claims processing.

Conduct payer-specific training for your major insurers. General COB rules provide the foundation, but experienced staff also need to know the quirks of your top 10 payers. Does Blue Cross Blue Shield require different coordination documentation than UnitedHealthcare? Does Medicare Administrative Contractor A process MSP claims differently than MAC B? Build this payer-specific knowledge through documentation of staff experiences, payer education sessions, and systematic tracking of what works with each major insurer.

Review COB denials during team meetings. When CO 22 denials occur, use them as teaching moments. During weekly or monthly staff meetings, select 2-3 actual denials, review what happened, walk through what should have been done differently, and discuss how to prevent similar errors. This ongoing education using real examples from your practice keeps COB awareness high and continuously reinforces proper procedures.

Update training when payer rules change. Insurance companies modify their coordination policies periodically. When a major payer changes their secondary claim submission requirements or modifies their MSP questionnaire, that warrants immediate training for all affected staff. Don’t assume people will pick up changes through casual communication. Formal updates with documented acknowledgment ensure everyone understands the new requirements.

Assess COB competency regularly. Include COB scenarios in competency evaluations for billing staff. Present hypothetical situations and evaluate whether staff determine payer order correctly, identify needed documentation, and follow proper workflows. This assessment identifies knowledge gaps requiring additional training and verifies that staff maintain competency over time as they encounter COB situations less frequently.

For larger organizations managing dozens of billing staff across multiple locations or shifts, standardized training approaches ensure consistent quality regardless of who provides the education. When training materials exist in documented, searchable formats rather than residing only in trainers’ knowledge, you can onboard new staff more quickly and provide refresher resources to experienced staff who need to verify specific details.

Organizations that excel at COB processing share a common characteristic: they’ve invested in building this expertise systematically rather than expecting staff to develop it informally through trial and error. The upfront investment in structured training pays dividends through lower denial rates, faster collections, and less staff frustration dealing with complex coordination scenarios.

Medicare Coordination of Benefits

Medicare coordination introduces unique complexity requiring special attention from billing teams. The rules differ from commercial insurance coordination, and federal oversight means mistakes can trigger more serious consequences than routine commercial claim denials.

Medicare beneficiaries often maintain other health insurance coverage. According to Kaiser Family Foundation data, approximately 23% of Medicare beneficiaries have supplemental coverage through employer-sponsored plans, and millions more have Medicaid or veterans’ benefits alongside Medicare. Determining whether Medicare pays primary or secondary in these situations follows specific federal rules that override standard coordination practices.

For Medicare beneficiaries aged 65 and older who continue working, the size of their employer determines coordination. Large group health plans—defined as covering employers with 20 or more employees—must pay primary to Medicare. This rule protects Medicare from covering costs that employer plans should rightfully pay for actively employed individuals. Once the beneficiary retires or moves to an employer with fewer than 20 employees, Medicare becomes primary.

The 20-employee threshold applies per location in some cases and per total company size in others, creating confusion about how to count employees. The determining factor is whether the employer is covered by the Medicare Secondary Payer provisions of federal law, which generally considers the total number of employees the employer had working in at least 20 weeks during the current or previous calendar year. Document this information carefully because incorrect Medicare Secondary Payer determinations can result in Medicare pursuing recovery if they pay primary when they shouldn’t have.

Medicare beneficiaries under age 65 who qualify due to disability follow different rules. Large group health plans for this population are defined as covering employers with 100 or more employees. These plans pay primary to Medicare during the first 30 months of Medicare eligibility. After 30 months, Medicare becomes primary. The higher threshold reflects federal policy giving employers with larger employee populations primary payment responsibility for disabled employees.

End-stage renal disease (ESRD) creates the most complex Medicare coordination scenario. When someone becomes Medicare-eligible due to ESRD, any existing group health plan remains primary for the first 30 months of Medicare eligibility. This 30-month coordination period gives the beneficiary time to adjust to Medicare coverage while protecting group health plans from immediately bearing full financial responsibility for ongoing dialysis and related services. After the 30-month coordination period expires, Medicare becomes the primary payer.

Track ESRD coordination periods carefully. Dialysis centers and nephrologists treating ESRD patients must maintain detailed records of each patient’s Medicare ESRD start date and coordinate benefits accordingly. Missing the transition from employer plan primary to Medicare primary means submitting claims to the wrong payer and receiving automatic denials that delay reimbursement for expensive treatment.

The Medicare Secondary Payer (MSP) questionnaire exists specifically to identify these coordination scenarios. Federal regulations require Medicare providers to complete MSP questionnaires for all beneficiaries and update them periodically—typically annually or whenever the beneficiary reports significant changes in employment, other insurance, or health status. The questionnaire asks about: current employment status, employer size, spouse’s employment and insurance, disability status, ESRD diagnosis date, liability insurance, no-fault insurance, and workers’ compensation coverage.

Submit MSP information to the Coordination of Benefits Contractor (COBC). CMS maintains a centralized database of Medicare coordination information updated by providers, insurers, employers, and beneficiaries. When you complete an MSP questionnaire and identify other insurance that should pay primary, submit that information to the COBC via their web portal or electronic reporting. This updates Medicare’s records so claims submitted by any provider for that beneficiary are processed with correct coordination.

Medicare conditional payments occur when Medicare pays a claim but later determines another payer should have been primary. In these situations, Medicare typically pays the claim conditionally, allowing treatment to proceed and providers to receive reimbursement. However, Medicare then pursues recovery from either the primary payer or, if necessary, the provider who billed incorrectly. Medicare’s conditional payment recovery efforts have increased substantially in recent years, making proper coordination more important than ever.

Avoid Medicare conditional payment situations by completing MSP questionnaires thoroughly and updating Medicare’s records when other coverage exists. While Medicare will generally pay conditionally to avoid delaying beneficiary care, providers shouldn’t rely on this as normal practice. The recovery process creates administrative burden, delayed revenue, and potential compliance risks if Medicare determines you habitually bill incorrectly.

Workers’ compensation, auto insurance, and other liability coverage always take precedence over Medicare for accident or injury-related treatment. Medicare specifically excludes coverage of services that other insurers are legally obligated to pay. When Medicare beneficiaries present for treatment of injuries potentially covered by these other sources, collect detailed information about the circumstances. If Medicare processes these claims first, they’ll later pursue recovery from the responsible payer or, if that’s unsuccessful, potentially from your organization for billing Medicare when you knew or should have known another payer was primary.

Medicare supplemental insurance (Medigap) coordinates differently than other coverage. Medigap policies are specifically designed to cover Medicare beneficiaries’ cost-sharing—deductibles, copayments, and coinsurance—rather than serving as primary coverage. When beneficiaries have Medigap, bill Medicare primary, then the Medigap policy automatically receives the Medicare crossover data and pays applicable secondary amounts. Providers don’t typically need to submit separate claims to Medigap carriers because crossover processing handles it automatically.

Medicare Advantage plans change coordination entirely. When beneficiaries enroll in Medicare Advantage (Part C), that plan becomes their primary Medicare coverage, and you follow that plan’s coordination rules rather than original Medicare rules. Medicare Advantage plans contract with CMS to provide all Medicare Part A and Part B coverage, so they pay as primary payers under their specific network and authorization requirements. If beneficiaries have other insurance alongside Medicare Advantage, coordinate according to that specific plan’s rules.

Document Medicare coordination decisions thoroughly. When you determine Medicare should pay secondary based on employment-based coverage, record the employer name, employer size, and beneficiary’s employment status. When you bill Medicare as primary, document why no other coverage exists or why Medicare should be primary despite other coverage. This documentation supports your decisions if questioned during audits or recovery efforts.

For practices serving large Medicare populations, Medicare coordination becomes a daily operational requirement rather than an occasional exception. Specialized training focused on MSP rules, systematic questionnaire completion processes, and clear documentation standards help ensure consistent handling across high claim volumes.

The Role of Technology in COB Management

Modern revenue cycle technology provides capabilities that support coordination of benefits processing, though technology alone doesn’t solve the fundamental challenges of COB. Understanding what technology can and can’t do helps organizations invest appropriately.

Eligibility verification platforms offer real-time coverage checks that identify multiple active insurances. When registration staff verify benefits electronically, the response often includes coordination indicators showing whether other coverage exists and sometimes even identifying the other payer. These immediate flags alert staff to probe deeper about additional coverage that might not be obvious from the insurance card alone. Most practice management systems integrate directly with eligibility vendors, making this verification nearly automatic for staff who understand how to interpret the responses.

But eligibility verification doesn’t determine payer order automatically. The system can tell you two active policies exist, but staff must still apply COB rules to determine which pays primary. Technology provides information; humans make determinations based on that information and additional details like patient age, employment status, and family relationships.

Claims scrubbing software validates coordination data before submission. These systems check whether the claim form includes Loop 2330 coordination information, verify that subscriber relationships make sense, and confirm that secondary claims include primary payer payment details. Good scrubbing catches data entry errors like transposed policy numbers or missing EOB attachments before claims reach payers. This prevents denials for technical errors unrelated to the actual COB determination.

Configure your scrubber’s rules for your specific needs. Out-of-box scrubber rules provide generic edits applicable to most practices, but you’ll achieve better results by customizing rules based on your organization’s common errors. If your team frequently forgets to attach primary EOBs when submitting secondary claims, configure a hard-stop edit that prevents transmission of any secondary claim missing that attachment. If certain payers routinely deny claims for specific coordination issues, build rules that flag those scenarios before submission.

Clearinghouses facilitate coordination by pulling primary payer remittance data and attaching it to secondary claims automatically. This electronic coordination of benefits (eCOB) capability eliminates the manual work of matching paper EOBs to secondary claims and reduces errors from missing or incorrect documentation. When your clearinghouse receives the 835 electronic remittance from the primary payer, it can automatically generate the secondary claim with proper coordination documentation and transmit it without manual intervention.

Practice management systems store multiple insurance policies per patient and allow staff to indicate payer order. Better systems provide dedicated fields for coordination-specific details like policy holder relationship, subscriber date of birth, and COB determination rationale. The challenge is ensuring staff actually use these fields consistently rather than burying important information in free-text notes that won’t flow to claim forms or be easily searchable later.

Configure your PMS to enforce coordination workflows. For example, set rules that prevent generating patient statements on accounts with multiple active insurances until all insurance processing completes. Flag accounts with dual coverage for special handling or second-person review before claim submission. Require staff to complete COB determination fields before the system allows claim creation. These automated controls prevent the process shortcuts that occur under time pressure.

Some practice management systems include COB rule engines that suggest payer order based on information entered during registration. These engines apply basic rules like birthday calculations or active/inactive determinations and propose which insurance should be billed first. Treat these suggestions as helpful guidance rather than definitive decisions, because the system can’t evaluate all the nuances that affect real-world coordination. Staff should review and confirm the suggestion rather than blindly accepting it.

Denial management systems help track and work COB-related denials systematically. These platforms categorize denials by reason code, route them to appropriate staff queues, track rework time, and monitor resolution rates. For CO 22 denials specifically, denial management systems can: prioritize them based on aging or dollar value, assign them to staff with COB expertise, track the documentation required to resolve them, calculate the delay impact on cash flow, and aggregate trends showing which staff members or which payers generate the most coordination errors.

Analytics and reporting tools identify COB patterns in your claims data. Monthly dashboards showing your CO 22 denial rate trends, denial rates by staff member, denial rates by payer, average days to resolve coordination denials, and revenue delayed by COB errors help leadership understand the scope of coordination challenges and measure improvement efforts.

But technology has clear limitations in COB processing. No system can interview patients to discover undisclosed coverage. No automated rule can read a divorce decree to determine court-ordered insurance responsibility. No algorithm can evaluate whether an injury is work-related and covered by workers’ compensation. These determinations require human judgment based on patient conversations, document review, and knowledge of complex scenarios that don’t fit simple if-then rules.

The most effective approach combines technology enablement with human expertise. Technology provides real-time information, enforces required workflows, reduces data entry errors, and automates routine processing. Humans apply COB rules to specific patient situations, make judgment calls about complex scenarios, resolve denials requiring research or appeals, and continuously improve processes based on patterns they observe. Healthcare organizations using TextExpander find this balance by using technology to make institutional knowledge instantly accessible while preserving the human expertise that complex COB scenarios require.

Organizations that struggle with coordination often expect technology to solve problems that actually require better training, clearer procedures, or more consistent documentation. Implementing new software doesn’t fix processes where staff don’t understand COB rules, don’t collect needed information during registration, or don’t follow established workflows. Fix the human and procedural elements first, then use technology to support and enforce those improved processes.

For coordination-heavy practices, technology becomes force multiplication for staff expertise. When your billing specialists understand COB thoroughly, technology helps them work faster and more consistently. When staff knowledge is weak, technology mainly produces more efficient errors. The organizations achieving the best results combine systematic staff training with smart technology deployment, ensuring people understand what needs to happen and technology makes executing those requirements easier.

Frequently Asked Questions About Coordination of Benefits

What does COB stand for in medical billing?

COB stands for Coordination of Benefits. It’s the process insurance companies use to determine which health plan pays first (primary payer) and which pays second (secondary payer) when a patient has multiple health insurance coverages. This ensures claims are paid correctly without duplicate payments or provider overpayment.

How do you determine primary vs. secondary insurance?

Primary vs. secondary insurance is determined using five core COB rules: the birthday rule (for dependent children, the parent with the earlier birthday in the calendar year has the primary plan), active vs. inactive employee rule (active employment coverage pays before COBRA or retiree plans), self vs. dependent rule (your own subscriber plan pays before a plan where you’re listed as a dependent), Medicare secondary payer rules (based on employment status and employer size), and Medicaid always pays last in any coordination scenario.

What is denial code CO 22?

Denial code CO 22 means “This care may be covered by another payer per coordination of benefits.” This denial indicates you submitted the claim to the wrong payer order. The insurance company is declining to process it and directing you to bill the correct primary payer first. CO 22 is one of the top 10 most common denial codes in medical billing.

Do you need the primary EOB to submit a secondary claim?

Yes, you need the primary payer’s Explanation of Benefits (EOB) attached to your secondary claim submission. Secondary payers require documentation showing what the primary payer allowed, paid, adjusted, and determined as patient responsibility before they can adjudicate their portion. Submitting a secondary claim without the primary EOB will result in a denial requesting that documentation.

What happens if you bill the wrong insurance first?

If you bill the wrong insurance first, the payer will deny the claim with reason code CO 22, indicating another payer should be primary per coordination of benefits. You must then submit to the correct primary payer, wait for their adjudication (15-45 days), receive their EOB, and only then bill the secondary payer with that documentation. This mistake typically adds 30-60 days to your collection timeline.

Is Medicare always the primary payer?

No, Medicare is not always primary. Medicare pays secondary when beneficiaries have active employer group coverage from employers with 20+ employees (for age 65+) or 100+ employees (for disability). Medicare also pays secondary to workers’ compensation, auto insurance, and no-fault insurance for accident-related care. Medicare only becomes primary when these other coverages don’t exist or after specific coordination periods expire (like the 30-month ESRD coordination period).

What is the birthday rule for coordination of benefits?

The birthday rule determines which parent’s insurance is primary for dependent children when both parents have coverage and are married and living together. The parent whose birthday (month and day only, not year) comes first in the calendar year has the primary plan for their children. For example, if Dad’s birthday is February 10 and Mom’s birthday is August 22, Dad’s insurance is primary regardless of which parent is older.

How long does coordination of benefits processing take?

Complete COB processing typically takes 30-75 days from initial claim submission to final payment. Primary payer adjudication takes 15-45 days for most private insurers, with post-service claims processed within 30 days under federal ERISA requirements. Secondary processing adds another 14-21 days. Medicare processes faster (often 14 days for electronic claims). Complex cases involving tertiary payers or multiple coordination issues can extend to 90+ days.

What is the 30-month coordination period for ESRD?

The 30-month coordination period for End-Stage Renal Disease (ESRD) is the timeframe during which a patient’s group health plan remains primary to Medicare. When someone becomes Medicare-eligible due to ESRD, any existing employer group health plan stays primary for the first 30 months of Medicare eligibility. After the 30-month period ends, Medicare automatically becomes the primary payer and the group health plan (if coverage continues) becomes secondary.

Can court orders override COB rules?

Yes, court orders override standard COB rules. When parents are divorced or legally separated, divorce decrees often specify which parent’s insurance must be primary for dependent children. These court-ordered insurance responsibilities supersede the birthday rule and other standard COB determination methods. Providers must document and follow the specific requirements stated in divorce decrees when billing for children of divorced parents.

What is a Medicare Secondary Payer questionnaire?

A Medicare Secondary Payer (MSP) questionnaire is a required form that identifies whether Medicare beneficiaries have other insurance that should pay before Medicare. Federal regulations require all Medicare providers to complete MSP questionnaires and update them periodically (typically annually or when circumstances change). The questionnaire asks about employment status, employer size, spouse’s insurance, disability status, ESRD diagnosis, and liability coverage to determine proper coordination.

How do you bill tertiary insurance?

To bill tertiary insurance (typically Medicaid in dual-eligible scenarios), first submit to the primary payer and receive their EOB, then submit to the secondary payer with the primary EOB attached and receive the secondary EOB, and finally submit to the tertiary payer with both previous EOBs attached showing all prior adjudication details. The tertiary payer reviews what both previous insurers paid and determines if any additional covered amounts remain.

What’s the difference between COB and duplicate billing?

COB (Coordination of Benefits) is the legitimate process of billing multiple insurers in proper sequence when a patient has multiple coverages. Duplicate billing is submitting the same claim to the same payer multiple times or billing multiple payers simultaneously without proper coordination—this is considered fraudulent. Proper COB follows established rules and sequences; duplicate billing violates billing regulations and payer contracts.

Do timely filing deadlines differ for secondary claims?

Yes, timely filing deadlines for secondary claims typically start from the primary payer’s adjudication date, not the original service date. Most secondary payers allow 90-120 days from when the primary payer processes the claim. However, requirements vary by payer—some accept secondary claims up to one year after service date if properly coordinated. Always verify each payer’s specific secondary claim filing requirements.

How does workers’ compensation affect COB?

Workers’ compensation always pays primary to all other coverage (including Medicare) for work-related injuries and illnesses. When patients present for treatment of work-related conditions, providers must bill workers’ compensation first, not the patient’s health insurance. Health insurance policies specifically exclude coverage for work-related injuries that workers’ compensation should cover. Proper documentation of injury circumstances is essential to determine whether workers’ comp applies.

What is the clean claim rate benchmark for COB accounts?